Ontario millennials need to save for over 20 years for down payment on a home: report

A real estate sign is displayed in front of a house in the Riverdale area of Toronto on Wednesday, September 29, 2021. THE CANADIAN PRESS/Evan Buhle

A real estate sign is displayed in front of a house in the Riverdale area of Toronto on Wednesday, September 29, 2021. THE CANADIAN PRESS/Evan Buhle

A new report shows house prices need to drop by more than $500,000 for millennials to be able to afford a home in Ontario.

Generation Squeeze, a charitable organization fighting for generational fairness in the country, recently released a 56-page reported called “Straddling the Gap 2022,” which looks at the disparity between home prices and earnings across the country.

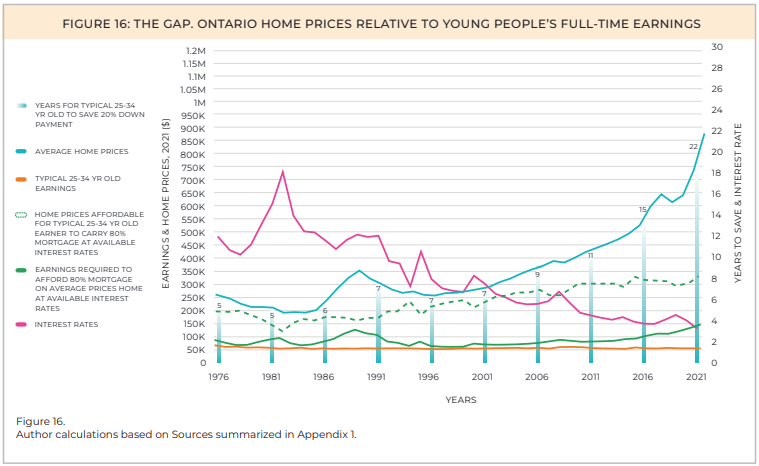

The study analyzes what Canada’s “primary goal” should be for home prices by looking at the gap between earnings and average home prices from 1976 until 2021, which was the last year available to procure data from the Canadian Real Estate Association (CREA).

After analyzing CREA’s data and comparing it to Statistics Canada’s data for annual income, the report concludes prices should stall “for many years ahead – or even continue to fall moderately.”

“The number of years of work required to save [for] a 20 [per cent] down payment on average priced homes has grown in alarming ways in many regions,” the report reads.

Across Ontario, average home prices were just shy of $900,000 last year.

Meanwhile, average income of Ontarians between the ages of 25 and 34 years has stayed nearly the same for decades, lingering at an average of roughly $50,000 a year. According to the latest data from StatsCan, the yearly income was $50,800 in 2020.

In order for millennials to buy a home in the province, the report says average home prices need to drop by $530,000, more than 60 per cent of the market value last year, for them to afford a mortgage that covers 80 per cent of the value.

Or, Ontario millennials will need to be earning $137,000 a year, which is roughly $85,000 more than what they are currently making on average.

A graph of Ontario's home prices relative to 25-to-34-year-olds full-time earnings. (Generation Squeeze)

A graph of Ontario's home prices relative to 25-to-34-year-olds full-time earnings. (Generation Squeeze)

“It takes 22 years of full-time work for the typical young person to save a 20 [per cent] down payment on an average priced home,” the report reads, which they say is 17 years longer than when “today’s aging population” were their age. The report did not clarify what age groups fall under this definition.

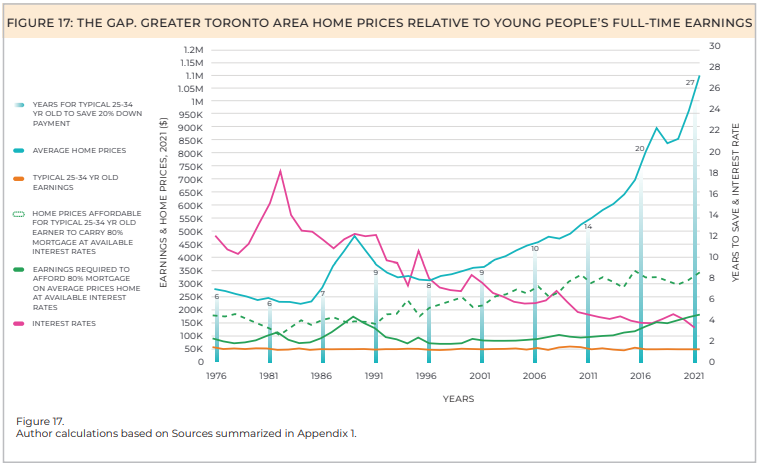

The lack of affordability in the Greater Toronto Area (GTA) is even steeper.

Those who have their sights set on owning a home in the GTA will have to save for an average of 27 years to make the same downpayment on an average-priced home. That is 10 years longer compared to the average amount of time across Canada.

Average annual incomes have remained at around $50,000 in the region, with StatsCan revealing 25 to 34-year-olds in the GTA raked in an average of $51,600 in 2020.

Meanwhile, average home prices in the region have soared to $1.1 million.

According to the report, these prices will have to fall by more than $750,000 for this age group to afford a mortgage that covers 80 per cent of the home’s value at current interest rates.

A graph of the GTA's home prices relative to 25-to-34-year-olds full-time earnings. (Generation Squeeze)

A graph of the GTA's home prices relative to 25-to-34-year-olds full-time earnings. (Generation Squeeze)

“Or typical full-time earnings would need to increase to $172,000/year – more than triple current levels,” the report notes.

Rent is also steep for those who cannot afford to buy, as the report notes it costs $20,148 a year for a two-bedroom apartment in the GTA in 2021.

With how much millennials make a year on average, rent takes up about 40 per cent of their income.

House prices in the GTA, however, are expected to drop slightly next year.

According to Re/Max Canada’s housing market outlook for 2023, prices are expected to fall by nearly 12 per cent to an average of just over $1 million.

Shopping Trends

The Shopping Trends team is independent of the journalists at CTV News. We may earn a commission when you use our links to shop. Read about us.

CTVNews.ca Top Stories

W5 Investigates

W5 Investigates A 'ticking time bomb': Inside Syria's toughest prison holding accused high-ranking ISIS members

In the last of a three-part investigation, W5's Avery Haines was given rare access to a Syrian prison, where thousands of accused high-ranking ISIS members are being held.

'Mayday!': New details emerge after Boeing plane makes emergency landing at Mirabel airport

New details suggest that there were communication issues between the pilots of a charter flight and the control tower at Montreal's Mirabel airport when a Boeing 737 made an emergency landing on Wednesday.

Federal government posts $13B deficit in first half of the fiscal year

The Finance Department says the federal deficit was $13 billion between April and September.

Canadian news publishers suing ChatGPT developer OpenAI

A coalition of Canadian news publishers is suing OpenAI for using news content to train its ChatGPT generative artificial intelligence system.

Weather warnings for snow, wind issued in several parts of Canada

Winter is less than a month away, but parts of Canada are already projected to see winter-like weather.

BREAKING

BREAKING Supreme Court affirms constitutionality of B.C. law on opioid health costs recovery

Canada's top court has affirmed the constitutionality of a law that would allow British Columbia to pursue a class-action lawsuit against opioid providers on behalf of other provinces, the territories and the federal government.

Cucumbers sold in Ontario, other provinces recalled over possible salmonella contamination

A U.S. company is recalling cucumbers sold in Ontario and other Canadian provinces due to possible salmonella contamination.

Nick Cannon says he's seeking help for narcissistic personality disorder

Nick Cannon has spoken out about his recent diagnosis of narcissistic personality disorder, saying 'I need help.'

Real GDP per capita declines for 6th consecutive quarter, household savings rise

Statistics Canada says the economy grew at an annualized pace of one per cent during the third quarter, in line with economists' expectations.

Montreal

-

Quebec trying to 'minimize' impact of health care cuts on services

Eliminating $1.5 billion in health care spending is likely to have an impact on services, but Quebec says it will try to 'minimize' it.

-

One woman killed, one hurt in armed robbery attempt southeast of Quebec City

One woman was killed and another was badly injured following an alleged armed robbery attempt at a clothing store southeast of Quebec City.

-

'Mayday!': New details emerge after Boeing plane makes emergency landing at Mirabel airport

New details suggest that there were communication issues between the pilots of a charter flight and the control tower at Montreal's Mirabel airport when a Boeing 737 made an emergency landing on Wednesday.

Ottawa

-

'Dude, Where's My Bus?' Ottawa man fed up with OC Transpo makes documentary exploring transit troubles

Gio Petti put together a documentary on OC Transpo, asking how we got here. How did a city that was once lauded as an example of how to do transit right, and that boasted some of the highest per capita transit ridership numbers in the country, become a system that now elicits so much frustration from users?

-

Ottawa police charge two adults, teenager following Orleans kidnapping and robbery

The Ottawa Police Service says two adults and a teenager are facing multiple charges following a kidnapping, robbery and extortion incident that happened last month in Orleans.

-

Ottawa to begin full enforcement of 3-item garbage limit on Monday: Here’s what you need to know

The City of Ottawa will begin the final phase of the graduated approach to enforcing the city’s new three-item garbage limit on Monday, leaving behind any extra items not in a yellow bag.

Northern Ontario

-

Another 50 cm of snow possible in the Sault as severe weather continues

Closures and cancellations are piling up in Sault Ste. Marie as a major winter storm continues for another day Friday.

-

Ongoing bed bug issue at a Timmins apartment building is 'like living in hell'

A battle with bed bugs continues at 217 Pine St. North in Timmins, according to a tenant who has lived there for a year and a half.

-

California man who went missing for 25 years found after sister sees his picture in the news

It’s a Thanksgiving miracle for one California family after a man who went missing in 1999 was found 25 years later when his sister saw a photo of him in an online article, authorities said.

Kitchener

-

One dead, another hurt in Cambridge shooting

Waterloo Regional Police are investigating a fatal shooting in Cambridge.

-

Police looking for missing teen last seen in Cambridge

Waterloo Regional Police are looking for information about the whereabouts of a missing teen.

-

Mother from Guelph, Ont. seeks answers following son's death in prison

Brody Robinson was found without vital signs in his cell at Millhaven Institution the evening of Oct. 29. He was 23-years-old.

London

-

Sarnia police lay charges after women wakes up to naked man in her home

An arrest has been made after a break and enter call in Sarnia where a woman woke up to a naked man in her home. Police said after investigating, officers were able to identify a 26-year-old man who was also wanted on an outstanding warrant in London.

-

Knights' Boulton hit with eight-game suspension

The left winger has been suspended eight games, retroactive to Nov. 23 against Saginaw, when he was handed a major penalty for slashing, along with a game misconduct.

-

'Shock, disappointment, and excitement': South Bruce not selected for nuclear waste project

Anja Vandervlies and Michelle Stein could hardly believe it when they heard South Bruce was not going to host Canada’s first permanent storage facility for nuclear waste.

Windsor

-

Breaking

BreakingBreaking Windsor man convicted on all counts by Chatham judge

The Windsor man charged in connection to the double fatal Retrofest collision has been convicted on all counts.

-

Windsor man charged in child pornography investigation

A Windsor man has been charged following a child pornography investigation.

-

Lakeshore announces new CAO

The Municipality of Lakeshore will have a new Chief Administrative Officer in the new year.

Barrie

-

50 cms of snow across central Ontario expected this weekend

Environment Canada has released snow squall warnings and watches for our region.

-

Individuals living in encampment in Barrie's south end given notice to vacate

Several police officers and city staff attended a homeless encampment in Barrie’s south end on Thursday morning to inform the individuals living there they would have to vacate the area.

-

Here are the school buses cancelled as wintry weather arrives

The winter weather has arrived, and with it come the first school bus cancellations of the season.

Winnipeg

-

Hanover School Division laying off 93 EAs due to confusion over funding

The Hanover School Division is laying off 93 educational assistants, citing an "unexpected loss of federal funding for Jordan's Principle programming."

-

Water main break causing Friday morning traffic delays in Winnipeg

Winnipeg drivers are being warned of traffic delays on Friday morning due to a water main break.

-

A tale of two downtowns: Restaurants opening and closing show complexity of downtown revival

Proposed developments and new businesses opening are fueling optimism for some on a revival of downtown Winnipeg, but some business owners say the present remains problematic.

Atlantic

-

Some closures, power outages in the Maritimes with first storm of the winter season

Parts of the Maritimes are experiencing their first winter storm on Friday with a messy weather system moving north from the eastern U.S.

-

Committee tracking mass casualty commission recommendations gives report on progress

The committee monitoring progress on the 130 recommendations made by the Mass Casualty Commission said progress is being made in three key areas, including gender-based intimate partner violence, access to firearms and police oversight.

-

Gas prices fall in N.S., P.E.I., increase slightly in N.B.

Gas prices change in all three Maritime provinces.

N.L.

-

'Who profits on hunger?': Inuit send pleading emails to minister about food costs

People in Nunavut and northern Labrador have been writing to Canadian government officials this year to say grocers were charging exorbitant prices despite receiving a federal subsidy.

-

As N.L. firm pivots, scientists say Canada's green hydrogen dreams are far-fetched

A Newfoundland energy company's embrace of data centres is raising doubts about eastern Canadian hopes of harnessing the region's howling winds to supply Germany with power from green hydrogen.

-

Canadian leads group pushing Vatican for zero-tolerance policy on abuse by clergy

An international group led by a Canadian is in Rome this week to push the Catholic Church to adopt a zero-tolerance policy on abuse by clergy.

Edmonton

-

Oilers rightly optimistic they can pull themselves into NHL playoff picture. Again

Hockey fans know the adage: U.S. Thanksgiving, while unofficial, serves as a great calendar marker in predicting which teams will make the National Hockey League playoffs.

-

ATV driver killed in crash on Sturgeon Lake Cree Nation

A 31-year-old man was killed in a crash on Sturgeon Lake Cree Nation on Thursday.

-

WEATHER

WEATHER Josh Classen's forecast: A few more cold and snowy days, then the deep freeze breaks

We'll close out November with two more frigid days and Sunday doesn't look much warmer.

Calgary

-

BREAKING

BREAKINGBREAKING Calgary Mayor Jyoti Gondek running for re-election

Calgary Mayor Jyoti Gondek has announced she will run for re-election in the next municipal election in 2025.

-

Multiple crashes reported on Deerfoot Trail

Calgary police say there are at least three major crashes on Deerfoot Trail on Friday morning as frigid overnight temperatures likely led to icy conditions in many areas.

-

Black Friday deals look to appeal to budget-friendly Calgary shoppers

Black Friday sales are in full swing as annual holiday shopping returns and Calgary retailers are competing harder than ever to coax budget-conscious shoppers into a deal.

Regina

-

Crown gives final remarks in Ruben Manz case as argument to jury concludes

The prosecution has presented their closing remarks against Ruben Manz to a 13-person jury, bringing an end to arguments before their sequestering.

-

Youngest roping duo looking for repeat performance at Agribition Rodeo

Kavis Drake, 18, and Denim Ross, 20, won the average in last year’s Maple Leaf Finals Rodeo team roping event at Agribition. The two were the youngest competitors in 2023 and are once again in their event this year.

-

Canada Post temporarily laying off striking workers, union says

The union representing Canada Post workers says the Crown corporation has been laying off striking employees as the labour action by more than 55,000 workers approaches the two-week mark.

Saskatoon

-

Ontario men arrested after Saskatoon police seize 16 kilos of meth, nearly $70K in cash

Saskatoon police say officers arrested three 20-year-old men Wednesday afternoon and seized nearly $70,000, in cash as well as various illicit drugs.

-

Extreme cold warning issued for Saskatoon

Environment Canada has issued an extreme cold warning for parts of central Saskatchewan, including Saskatoon, on Thursday.

-

Sask. forecasting $743.5M deficit in mid-year financial report, up $470.5M from budget

The provincial government says increases to crop insurance claims later in the growing season are a main reason for Thursday’s mid-year deficit forecast of $743.5 million, which is up more than $470 million from the budget.

Vancouver

-

Surrey Police Service officially takes over from the RCMP after years-long saga

The years-long saga over who will police the city of Surrey has reached its final chapter.

-

How changing catch-and-release fishing practices can boost salmon survival

A study has found catch-and-release sportfishing practices that leave salmon with injuries, particularly to their eyes, cause higher mortality than earlier research suggested.

-

BREAKING

BREAKING Supreme Court affirms constitutionality of B.C. law on opioid health costs recovery

Canada's top court has affirmed the constitutionality of a law that would allow British Columbia to pursue a class-action lawsuit against opioid providers on behalf of other provinces, the territories and the federal government.

Vancouver Island

-

How changing catch-and-release fishing practices can boost salmon survival

A study has found catch-and-release sportfishing practices that leave salmon with injuries, particularly to their eyes, cause higher mortality than earlier research suggested.

-

BREAKING

BREAKING Supreme Court affirms constitutionality of B.C. law on opioid health costs recovery

Canada's top court has affirmed the constitutionality of a law that would allow British Columbia to pursue a class-action lawsuit against opioid providers on behalf of other provinces, the territories and the federal government.

-

Avian flu case discovered in Greater Victoria, officials confirm

The Canadian Food Inspection Agency (CFIA) has confirmed a case of avian flu has been detected in Greater Victoria, on the Saanich Peninsula.